Islamic Financial Transactions: Ṣīgha, Qabḍ, and the Validity of Contracts

The Wording of the Transaction (Ṣīgha)

As previously discussed, mutual satisfaction (riḍā) between contracting parties forms the essential foundation of a valid transaction in Islamic law. However, to ensure that this satisfaction is recognised and verifiable, it must be manifested through explicit expression. This formal expression is referred to as ṣīgha—the declarative wording that constitutes the offer and acceptance in a contract.

The ṣīgha comprises two principal components:

- Ījāb (offer): the initial declaration by one party expressing willingness to enter into a transaction.

- Qabūl (acceptance): the corresponding affirmation by the other party, signifying their agreement to the proposed terms.

For the contract to be valid, the ījāb and qabūl must be articulated using clear and unambiguous language that corresponds directly to the nature of the intended transaction. This articulation may take various forms:

- Verbal statements

- Written communication

- Other conventionally recognised modes of expression (e.g., electronic signatures, digital confirmation), provided these are accepted in the context of the transaction.

While the dominant view in the Shāfiʿī school holds that validity depends on express verbal or written terms[1], Imām Mālik's position is more inclusive. He maintains that any culturally accepted form of expression—even non-verbal actions that unambiguously convey mutual agreement—may suffice. Imām al-Nawawī notably endorses[2] this view, describing it as stronger in evidence and more aligned with the overarching objective of upholding mutual consent. Scholars such as al-Baghawī, al-Mutawallī, and al-Ruʾyānī concur, with al-Mutawallī even asserting that legal verdicts (fatāwā) should be issued based on this broader understanding[3].

The underlying principle is not merely the formality of speech but the clear manifestation of mutual satisfaction. As the Qur’ān and Sunnah do not rigidly prescribe the specific mode of expression, flexibility is afforded so long as the transaction remains free of ambiguity and both parties are genuinely consenting[4].

Additional legal conditions related to ṣīgha include the following:

- The terms must be mutually consistent and free from internal contradiction.

- The interval between offer and acceptance must not be excessive. If the parties are physically present, the acceptance must occur before they part company. In remote transactions, the acceptance must occur within the same session or context as the received offer.

- Continuity of legal capacity (ahliyyah) is also essential: both parties must retain the ability to contract at the time of both ījāb and qabūl. If the initiating party becomes legally incapacitated (e.g., through insanity, death, or loss of legal authority) before acceptance, the transaction is rendered invalid[5].

In sum, ṣīgha serves as the formal mechanism that enshrines the spirit of mutual consent in a legally recognisable framework, ensuring transparency, accountability, and fairness in all valid Islamic commercial transactions.

Transfer of Possession (Qabḍ)

In Islamic jurisprudence (fiqh), qabḍ refers to the act of transferring the subject matter of a transaction in a manner that enables the recipient to utilize, benefit from, or control the item. The concept of qabḍ is critical in validating transactions such as sales (bayʿ), leasing (ijārah), and other financial agreements, ensuring that ownership rights are fully realised through effective possession.

The method by which qabḍ is achieved varies depending on the nature and characteristics of the item being transacted[6]. Classical jurists generally categorise qabḍ into three broad forms:

- Possession of Immovable Property

For items that cannot be physically moved—such as land, houses, or fruits still attached to trees—possession is deemed complete when:

- The seller vacates the property, removing any personal claims or barriers.

- The buyer is granted unhindered access and control over the property.

- Handing over the keys to a property, or transferring legal documents that establish ownership and access, also constitutes valid qabḍ in such cases.

- Possession of Movable Tangible Goods

For items that are easily portable, such as: Books, Clothing, Grocery items

The transfer of possession is completed through physical handover. Actual delivery into the hands of the buyer or their agent finalises the transaction. This direct conveyance ensures clarity, prevents disputes, and fulfills the requirement of full ownership transfer.

Movable Items Requiring Relocation (Manqūlāt Ghayr Maḥsūsa):

For movable items that cannot be directly handed over due to their size or nature—such as large furniture or heavy goods—the transfer is completed when the items are physically moved (naql) and delivered (taslīm) to the other party.

For commodities that are sold based on measurement, weight, or count—such as: Grains, Oil, Currency, Livestock (sold by number)

Qabḍ is considered valid only after the items have been properly measured, weighed, or counted as per the nature of the item and as per the terms of the contract[7]. This ensures that the quantity and specification agreed upon are clearly defined, thereby eliminating ambiguity (gharar) and fulfilling contractual certainty (yaqīn).

Different Types of Possessions

- Liability-Based Possession (Yad Ḍamān)

Also known as liability-based possession, yad ḍamān imposes full responsibility on the possessor for the held property, regardless of negligence or fault. If the property is damaged, destroyed, or lost under their custody, the possessor must compensate for it—either by replacing the item, paying its value, or relinquishing their claim.

Examples include:

- Sale Transactions: If an item sold is damaged before delivery to the buyer, the seller—who retains possession—remains liable. According to the majority opinion, the seller cannot claim the sale price because the transaction is not fully executed until qabḍ (effective transfer) occurs.

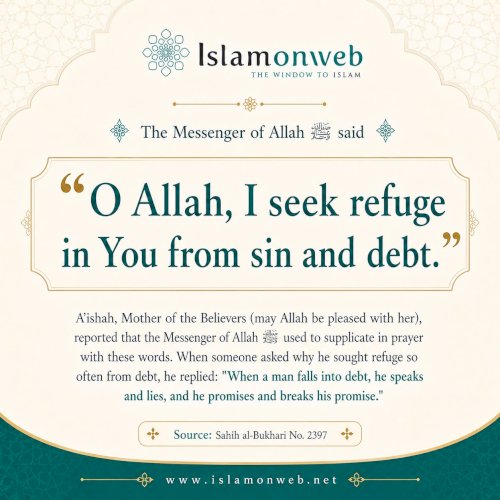

- Loan Transactions (‘Āriyya): In gratuitous loans, the borrower bears the liability. Even if the borrowed item perishes without the borrower's fault, they are obligated to compensate.

- Debt (Qarḍ): A debtor remains fully liable for the borrowed sum. If the borrowed asset is lost while in the debtor’s possession, repayment remains due, irrespective of circumstances.

Thus, the general legal maxim (qāʿidah fiqhiyyah) applies:

"The object remains the liability of the seller (or possessor) until actual possession (qabḍ) is completed by the buyer (or transferee)."

- Trusteeship-Based Possession (Yad Amāna)

In contrast, trusteeship-based possession (yad amāna) imposes liability only if the possessor acts negligently, misuses the property, or violates the terms of trust. If the loss occurs due to natural disasters, theft without negligence, or unforeseen events, the possessor is not required to offer compensation.

Examples of yad amāna include:

- Partnerships (Mushāraka, Muḍāraba): Each partner or managing party holds the other's property in trust. Losses due to market conditions, not mismanagement, are borne collectively according to agreed ratios.

- Agency (Wakāla): An agent handling goods on behalf of a principal is not liable for losses unless proven negligent.

- Deposits (Wadīʿa): A person safeguarding another's property without compensation (a depositary) is only liable if they misuse, neglect, or act beyond their authorised limits.

Hence, management under amāna (trusteeship) is fundamentally based on good faith and mutual benefit, not on absolute liability.

To sum up. in Islamic financial ethics:

- Yad ḍamān holds the possessor strictly liable, regardless of fault.

- Yad amāna shields the possessor from liability unless negligence, misconduct, or breach of trust occurs[8].

Recognising the distinction between these two types of possession ensures fairness, protects property rights, and prevents unjust enrichment or undue risk transfer in Islamic financial transactions.

Validity of Transactions and Related Rules

In Islamic commercial law, transactions (ʿuqūd) are evaluated based on their adherence to essential components (arkān) and legal conditions (shurūṭ). A transaction that fulfills its fundamental elements and complies with all requisite stipulations is classified as ʿaqd ṣaḥīḥ (valid contract). Such contracts are legally enforceable, and their consequences—such as transfer of ownership (milk) and liability—take effect upon execution[9].

Transactions that do not meet these criteria are categorised either as ʿaqd bāṭil (void contract) or ʿaqd fāsid (voidable contract), depending on the nature and extent of the violation. While most of the scholars hold the view that both ʿaqd bāṭil and ʿaqd fāsid are synonyms and can be denoted for any kind of invalid contracts, Hanafi scholars defines them separately as follows.

A bāṭil contract is one that is invalid from the outset due to the absence of essential elements or because it involves a prohibited object or purpose. For instance, contracts involving the sale of ḥarām (prohibited) items such as alcohol or pork, or contracts lacking mutual consent, fall under this category. Such contracts have no legal standing, and no rights or obligations emerge from them.

A fāsid contract, on the other hand, is one that is initially valid in its core structure but rendered defective due to a breach of ancillary conditions or improper implementation. For example, a sale in which the price or the object sold is not clearly defined is considered fāsid.

Legal Implications of Fāsid Contracts

- Under the Shāfiʿī and Ḥanbalī schools: No ownership (milk) is transferred through a fāsid transaction. Even if physical possession (qabḍ) takes place, both parties are obliged to return the exchanged wealth to annul the contract.

- Under the Ḥanafī school:

- If qabḍ has not occurred, no ownership is transferred, and the wealth must be returned.

- If qabḍ is completed, a temporary ownership (milk muʿaqqat) is established.

- If the item is transformed or used in another transaction, ownership becomes permanent (milk dā’im), and the option to annul the contract is forfeited[10].

- According to the Mālikī school: If the option to reclaim is forfeited or lost, ownership is deemed to have been established, even if the original transaction was defective[11].

- Participating in fāsid transactions is considered prohibited (ḥarām)[12] due to the violation of Sharīʿah conditions.

- However, in cases of extreme necessity (ḍarūra)—such as life-threatening circumstances or absolute scarcity of lawful alternatives—fāsid contracts may be deemed temporarily permissible[13] (mubāḥ) under the legal maxim:

“Necessities permit the prohibited” (al-ḍarūrāt tubīḥ al-maḥẓūrāt).

Conclusion

The classification of contracts into ṣaḥīḥ, fāsid, and bāṭil reflects the ethical priorities of Islamic finance. It preserves clarity, protects rights, and deters exploitative or careless conduct in commercial dealings. A sound understanding of these categories is essential for upholding the integrity of Islamic transactions and ensuring justice in financial practices.

Reference:

[1] Ibn Ḥajar al-Haytamī, Tuḥfat al-Muḥtāj, vol. 4, p. 217

[2] Imām al-Nawawī, Rawḍat al-Ṭālibīn, vol. 3, p. 339

[3] Imām al-Nawawī, Sharḥ al-Muhadhdhab, vol. 9, p. 163

[4] Imām al-Nawawī, Rawḍat al-Ṭālibīn, vol. 3, p. 339

[5] Imām al-Nawawī, Sharḥ al-Muhadhdhab, vol. 9, p. 169

[6] Kuwait Encyclopedia of Fiqh, vol. 32, p. 259; Imām al-Nawawī, Sharḥ al-Muhadhdhab, vol. 9, p. 275

[7] ʿIzz al-Dīn ibn ʿAbd al-Salām, Qawāʿid al-Aḥkām fī Maṣāliḥ al-Anām, vol. 2, p. 84

[8] Muḥammad Najīb al-Muṭīʿī, Takmīlat al-Majmūʿ, vol. 14, p. 158, Kuwait Encyclopedia of Fiqh, vol. 28, p. 258

[9] Imām al-Nawawī, Sharḥ al-Muhadhdhab, vol. 1, p. 32

[10] Imām al-Nawawī, Rawḍat al-Ṭālibīn, vol. 3, p. 408

[11] al-Kāsānī, Badāʾiʿ al-Ṣanāʾiʿ fī Tartīb al-Sharāʾiʿ, vol. 5, pp. 299–304

[12] al-Sarakhsī, al-Manthūr fī al-Qawāʿid al-Fiqhiyya, vol. 3, p. 16, al-Mardāwī, al-Inṣāf fī Maʿrifat al-Rājiḥ min al-Khilāf, vol. 4, p. 473

[13] al-Sharbinī, Mughnī al-Muḥtāj, vol. 2, p. 378, al-Sarakhsī, al-Manthūr fī al-Qawāʿid al-Fiqhiyya, vol. 1, p. 355

Disclaimer

The views expressed in this article are the author’s own and do not necessarily mirror Islamonweb’s editorial stance.

Related Posts

Leave A Comment